Insights

Quarterly Commentary

3Q 2020

As the fourth quarter unfolds, the market seems to be walking a tight rope – stocks are holding up well, yet it seems that so much could go wrong. The apparent hazards cannot be ignored but ultimately investors must raise their eyes to the horizon and take one step at a time. Potential positive outcomes get less attention as they don’t make for good headlines. It is natural to worry most about the things we can’t control. In the current environment, we are alleviating stress by deepening our understanding of the risks, by focusing on how specific sectors and companies are navigating myriad challenges and by imagining alternative scenarios that might unfold.

We believe that the economy will continue to recover. Our base case is a resumption of day-to-day activities that eventually includes air travel, dining out, trips to the ballpark and regular visits to the gym. Progress will not occur in a straight line, yet we will persevere and in the not too distant future life will return to something resembling normal.

While the stock market is outwardly buoyant, performance at the sector level is askew by historic proportions. If the recovery unfolds even close to how we expect, the market’s current favorites may step back, with new leaders emerging from among today’s forgotten stocks.

Putting the risks into context

HEALTH - Reports of SARS-CoV-2 outbreaks and increasing case counts are rekindling fears of exposure and triggering flashbacks of last spring’s lockdown. Yet more widespread testing and new targeted treatments are reducing mortality rates. Societal and economic costs of lockdowns are increasingly evident. Among the unintended effects, global poverty may increase in 2020 for the first time since 1998. Many governments are adopting more nuanced strategies to manage the pandemic. We believe both treatments and policy will continue to improve.

ECONOMY – The recovery overall has surpassed most economists’ early projections; however, significant challenges remain. Hotels, airlines, and movie theaters are only in the early innings of a revival. Many individuals and state/local governments are strapped for cash. Without further fiscal stimulus, there will be unnecessary permanent damage. We are optimistic that it is only a matter of time before additional federal aid is forthcoming.

POLITICS - Fair elections and peaceful transfers of power are cornerstones of democracy. The worst outcome for the market would for either or both of these principles to be (or appear to be) violated. Less extreme, but concerning to many, is a potential roll-back of the 2017 Tax Cut and Jobs Act should Biden win. However, Wall Street may be able to cope with higher taxes if accompanied by more fiscal stimulus and infrastructure investment.

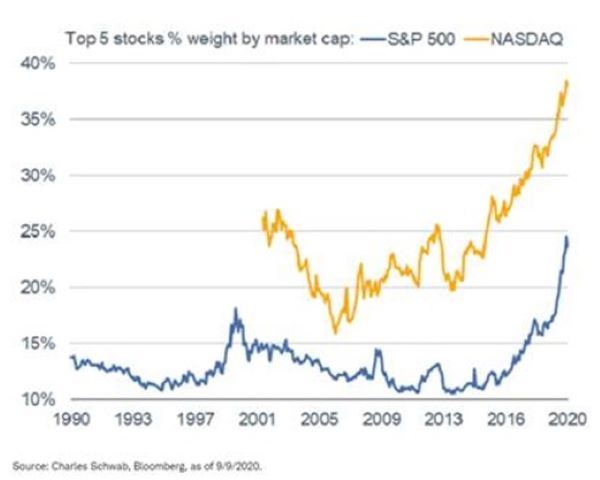

MARKET –The five largest tech stocks now account for about 25% of the S&P 500 and 20% of the value of all US stocks. Facebook, Amazon, Apple, Microsoft and Google have become even more essential during the pandemic, and their stocks have come to be viewed as safe havens in an uncertain world. Investors have bid up the shares to the moon -- today’s lofty share prices fully value profits anticipated to be earned many years into the future. Even a small uptick in inflation will reduce the value of those future profits with a chilling effect on the share prices. At the same time, regulators around the world have their eyes keenly trained on big tech, raising the possibility of antitrust action.

Notable divergences (year-to-date through September 30th):

- Average return for five largest tech stocks (FAAMG) – up 40%

- Average large US stock – down 5%

- Average US stock (all sizes) – down 12%

Unprecedented market concentration:

Seeking value in an inflecting economy

Investors tend to gravitate to what has recently “worked.” Market-cap weighted indexes automatically hold more of the winners and less of the losers. Following this strategy works when the future looks like the recent past, but less well when the winners’ valuations border on the crazy or when there is a change in the investing climate. This may be the case now. If one believes, as we do, that better times are ahead, it makes sense to be looking at sectors that have lagged and would be positively exposed to a continued recovery.

Financials fit this bill. Banks, in particular, are highly cyclical and the benchmark KBE bank index fell 36% over the first three quarters of the year. To be sure, the group’s profits have come under pressure from a combination of lower interest rates and a new accounting rule that greatly accelerated, and possibly exaggerated, reserving for potential loan losses that may arise as the economy slowly regains its footing. Collectively, US banks’ loan loss reserves now approach $250 billion, near the peak registered during the Great Financial Crisis. To date, however, actual charges for defaulted loans are tracking at normal levels. While that may change as stimulus payments wane, so far it seems that perception is out of step with reality. Bank stock valuations imply that a deepening recession lies ahead. That is at odds with our own expectations – and is inconsistent with how the rest of the stock market is behaving.

Similarly, smaller companies have suffered more than large as the slowdown has disproportionately hurt their prospects and pressured their balance sheets. This is reflected in their poor performance this year – the Russell 2000 trailed the S&P 500 by 14% at the end of September. We cannot predict how or when this unusually wide gap will narrow – however it reinforces our interest in identifying well-managed and well-positioned smaller companies poised to recover along with the economy.

Conclusion

The pandemic is testing our fortitude. We have seen how our lives can be upended when the economy is shut down. Market forces continue to shift as the recovery takes shape. In such times, one may be tempted to seek comfort in consensus thinking or may be paralyzed by uncertainty. There is no doubt that 2020 has been a difficult year, yet where others only see risk, we see opportunities.